**Ideon is the company formerly known as Vericred. Vericred began operating as Ideon on May 18, 2022.**

This is the second of three posts on this subject

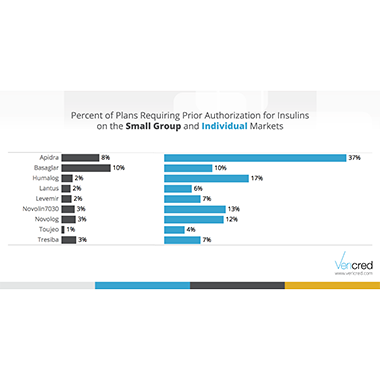

In this blog series for Diabetes Awareness month, we are exploring how the medications used to treat diabetes are covered by ACA health insurance plans. In our last post, we showed that many plans exclude entire classes of diabetes medication. In this post, we will explore the prevalence of prior authorization requirements with a focus on insulin.

Prior authorization is a tool that formularies can use to control access to certain medications. Although drugs with a prior authorization requirement are covered, providers are often hesitant to go through the approval process. From a patient perspective, this can be similar to the drug not being covered. The data science team at Vericred investigated the coverage for diabetes medications under ACA small group and individual plans to see how often they are subjected to prior authorization requirements.

The results show that prior authorization requirements are quite common. The majority of plans require it for at least one of the 53 diabetes medications studied. All nine medications in the insulin class require prior authorization from at least some plans. Individual plans are more likely to require it than are small group plans. The most striking example of this is Apidra – 37% of the individual plans that cover this drug require prior authorization compared to an 8% of small group plans.

Consumers with diabetes and employers shopping for insurance plans need to look carefully at the formulary information for the plans they are considering. Even if a drug is covered, some plans place additional requirements like prior authorization that can limit access to certain medications.