VeriStat: How Deductibles for Silver Plans Vary by State: Part III

Published on June 26, 2018

By: Abby Grunewald

**Ideon is the company formerly known as Vericred. Vericred began operating as Ideon on May 18, 2022.**

This is the final post of a three-post series on this subject.

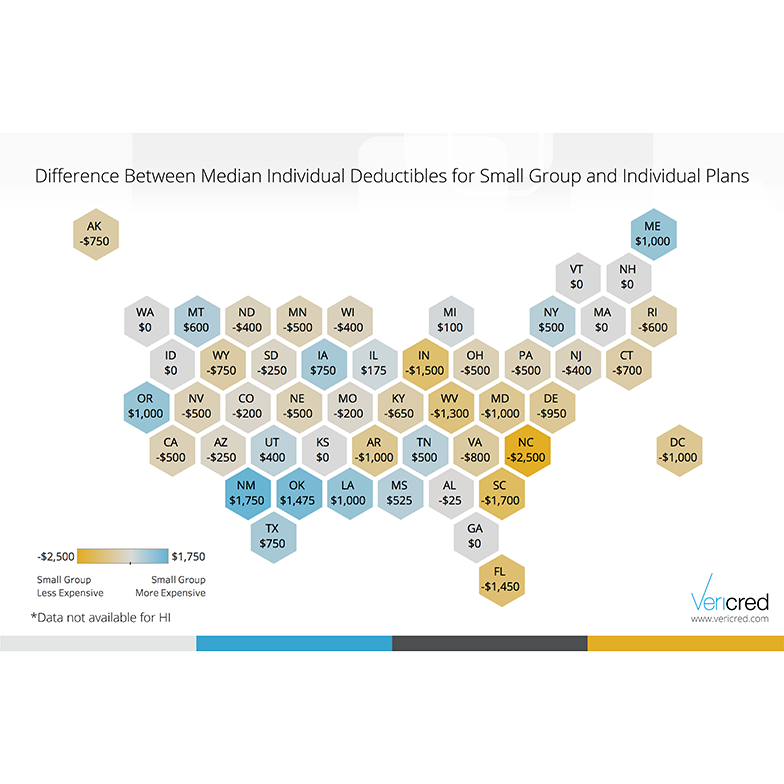

To increase transparency, plans offered under the ACA are given metal levels based on how the cost of care is split between an individual and their health plan. Silver plans must cover 70% of a typical population’s healthcare costs, but plans can use a wide variety of different cost-sharing structures to arrive at this 70%. The deductible – the amount the individual must cover before their plan begins to pay—is one factor that can make a big difference to out-of-pocket costs.

In our last two posts, we examined the deductibles for small group silver plans and found that there is substantial variation in both the median deductible between states and the range of deductibles within each state. In this post, we will compare states’ median deductibles in the small group market to those on the individual market.

The data science team at Vericred analyzed the difference between the deductibles for small group and individual silver plans to see how this relationship varies by state. The results range from the median small group deductible being $2,500 less expensive in North Carolina to $1,750 more expensive in New Mexico. For the majority of states, the small group market has less expensive deductibles than the individual market, however, there are 14 states where the small group deductibles are more expensive. Small employers considering whether to offer group health insurance should consider which aspects of cost-sharing matter most to their employees and how cost-sharing differs between the individual and small group markets in their state.