As value-based care accelerates, regulatory expectations intensify, and competitive pressure increases in 2026, organizations managing provider networks can no longer rely on intuition, spreadsheets, or retrospective reviews. The ability to turn raw claims data and provider information into actionable intelligence now determines whether networks control costs, meet adequacy standards, and deliver high-quality member experiences.

At its foundation, provider network analytics transforms massive volumes of data—millions of claims, provider profiles, utilization patterns, and access metrics—into clear insight about how networks actually perform. Modern analytics goes far beyond counting providers or reviewing quarterly reports. It measures cost efficiency, quality outcomes, access, utilization, and competitive positioning simultaneously, enabling organizations to design and optimize networks with precision rather than guesswork.

Organizations with advanced network analytics capabilities consistently outperform peers. They identify high-performing providers, predict adequacy gaps before they become regulatory violations, reduce medical costs through smarter network design, and adapt rapidly to changing market dynamics. Those without analytics remain stuck in reactive cycles—addressing issues only after members complain, regulators intervene, or costs escalate.

This guide explores what healthcare provider network analytics encompasses, why it has become a competitive necessity in 2026, and how modern analytics platforms and API-driven data infrastructure allow organizations to optimize networks in minutes rather than months. In a healthcare landscape where network performance directly drives financial results and member outcomes, analytics is no longer a technical upgrade—it is a strategic imperative.

Why Network Analytics Is Now a Competitive Necessity

Health plans processing millions of claims annually recognize analytics as strategic differentiator between market leaders and laggards. Organizations with advanced network analytics capabilities identify high-performing providers, predict network adequacy gaps before regulatory violations occur, and optimize provider mix for cost-effective care delivery. The strategic question facing payers, ACOs, and benefits technology platforms: continue manual provider analysis consuming staff time without delivering actionable insights, or adopt comprehensive analytics transforming data into competitive advantage?

Traditional network management relies on quarterly performance reviews, spreadsheet-based provider comparisons, reactive adequacy monitoring, and subjective recruitment decisions influenced by relationships rather than objective data. This approach produces networks with unknown cost efficiency, provider performance gaps invisible until members complain, regulatory compliance risks from inadequate monitoring, and missed opportunities for strategic network optimization.

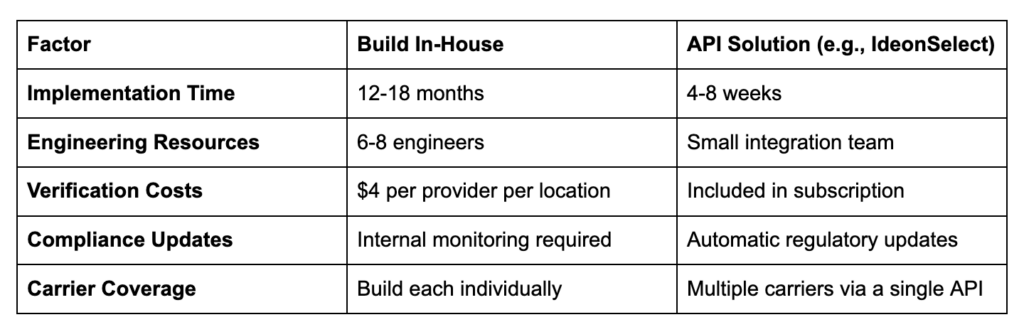

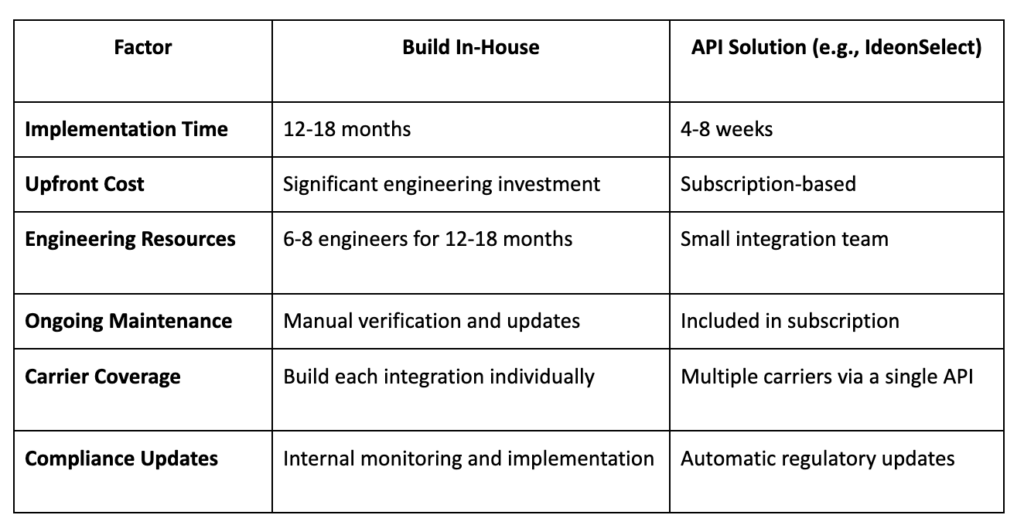

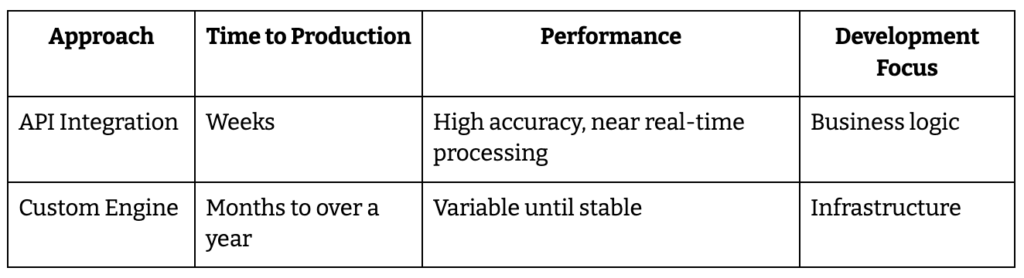

Healthcare provider network analytics operates differently. Comprehensive platforms enable automated performance measurement across cost, quality, and satisfaction metrics, real-time network adequacy monitoring with predictive gap forecasting, competitive intelligence revealing market positioning and provider overlap, and AI-powered recommendations for network design and provider recruitment. Organizations face infrastructure decision: build analytics capabilities internally requiring significant data engineering investment and 12-18 months development, or leverage existing platforms and API infrastructure deploying in weeks.

Network analytics evolved from nice-to-have reporting to competitive necessity throughout 2026 as value-based care adoption accelerates and regulatory scrutiny intensifies.

What Is Healthcare Provider Network Analytics?

Healthcare provider network analytics: The systematic use of data science, statistical analysis, and business intelligence tools to evaluate provider network performance, optimize network composition, and improve healthcare delivery outcomes through data-driven insights.

Healthcare provider network analytics encompasses provider performance measurement across multiple dimensions including cost efficiency metrics revealing total cost of care per episode, quality indicators tracking clinical outcomes and adherence to evidence-based protocols, patient satisfaction scores measuring member experience, and utilization pattern analysis identifying appropriate versus unnecessary care. Network utilization analysis examines member access patterns showing which providers members actually use versus directory listings, appointment availability tracking wait times and access barriers, referral flow mapping revealing where care happens within and outside networks, and service gap identification highlighting unmet member needs.

Competitive intelligence capabilities provide comparative network positioning showing how organization’s network compares to competitors, market share analysis quantifying provider relationships and member volume, competitor provider network mapping revealing overlap and differentiation opportunities, and strategic recruitment targeting based on competitive gaps. Predictive modeling forecasts network adequacy gaps before regulatory violations occur, cost trend predictions enabling proactive contract negotiations, member needs forecasting based on demographic and utilization shifts, and provider performance trajectories identifying improving versus declining providers.

Claims data analysis processes pattern recognition across millions of claims revealing efficiency opportunities, outlier detection flagging unusual cost or quality patterns requiring investigation, episode grouping enabling accurate cost comparisons, and risk adjustment ensuring fair provider performance comparisons. Organizations transform manual, time-consuming provider analysis requiring weeks of spreadsheet work into automated, self-service analytics delivering insights in three clicks rather than three weeks.

Healthcare provider network analytics sits as strategic decision-making layer for network design and optimization rather than simple reporting function. It provides foundation for value-based care arrangements and risk management by quantifying provider performance objectively. Analytics creates critical infrastructure for competitive positioning and member satisfaction by identifying network strengths and gaps. The function proves essential for regulatory compliance and network adequacy reporting by continuously monitoring rather than scrambling before audits.

Why Healthcare Provider Network Analytics Matters

network decisions that replace guesswork with evidence-based provider selection and network design. Organizations using advanced analytics platforms build high-performance networks in minutes rather than months by simulating hundreds of network configurations and selecting optimal combinations. Leading platforms explore 100+ network configurations per market testing various provider combinations against strategic objectives, dramatically accelerating what previously required months of manual analysis.

Cost containment delivers measurable financial impact through optimized network design. Organizations achieve typical 10% reduction in total medical cost through strategic network optimization balancing access, quality, and cost objectives. These savings compound annually as refined networks steer members to high-value providers. Regulatory compliance shifts from reactive firefighting to proactive adequacy monitoring preventing violations before regulatory agencies identify issues, avoiding penalties and protecting plan ratings.

Members and patient care quality improves when better provider matching based on outcomes data connects members to appropriate specialists. Equitable access to high-quality, affordable care results from analytics revealing geographic and specialty gaps requiring attention. Reduced wait times emerge from capacity analysis identifying providers with availability versus those with 6-month backlogs. Network optimization focusing on member needs rather than provider convenience creates superior experiences.

Provider organizations understand network performance and market position through analytics showing comparative performance against peers. Identifying opportunities for improved contracting and partnerships becomes possible with objective performance data. Data-backed negotiations with payers based on quality and efficiency metrics rather than relationship leverage create win-win agreements. Transparency enables collaborative improvement rather than adversarial contracting.

Market intelligence transforms strategic planning when organizations access comprehensive claims datasets covering 300 million beneficiaries and 10 billion claims enabling market and cohort intelligence at unprecedented scale. Complete Medicare, Medicaid, and Commercial data visibility reveals competitive positioning, market share trends, and expansion opportunities invisible with limited data access. Analytics platforms processing millions of claims identify patterns and opportunities manual analysis would never discover.

Core Components of Network Analytics Systems

Comprehensive Claims Data Integration

Access to Medicare, Medicaid, and Commercial claims datasets provides foundation for meaningful analytics. Platforms with over 2 million physician profiles offering national and regional performance benchmarks enable accurate comparisons. Multi-source data aggregation creates holistic provider performance views impossible with single payer data. High-confidence data results from rigorous cleaning and standardization processes eliminating garbage-in-garbage-out problems plaguing internally-built analytics.

Provider Performance Analytics

Cost and quality metrics include provider efficiency scores comparing total cost of care against peers, effectiveness ratings measuring clinical outcomes for similar patient populations, and total cost of care calculations accounting for downstream services triggered by initial treatment decisions. Clinical activity tracking reveals top procedures providers perform most frequently, conditions they treat successfully, medications prescribed indicating specialty focus, and actual specialties served versus claimed credentials.

Peer group comparisons enable benchmarking against similar providers in same markets controlling for patient mix and local market factors. Patient satisfaction measurements incorporate CAHPS scores from official surveys, member feedback from plan-administered assessments, and experience ratings from various touchpoints. These comprehensive performance views replace limited internal data with market-wide intelligence.

Network Adequacy and Access Analysis

Geographic access evaluation ensures compliance with time and distance standards mandated by CMS, state regulators, and accreditation bodies. Provider-to-member ratio calculations by specialty and county quantify whether sufficient provider capacity exists for member populations. Panel capacity monitoring tracks “accepting new patients” status preventing directories listing providers unavailable to new members. Appointment wait time assessment reveals actual access barriers members face versus theoretical network adequacy on paper.

Competitive Intelligence and Market Analysis

Competitor network composition analysis identifies which providers participate in rival networks revealing differentiation opportunities. Provider overlap identification shows where multiple plans compete for same providers versus exclusive relationships. Market share analysis quantifies claims volume and member attribution across competing networks. Claims volume insights across IDN, ACO, and GPO relationship hierarchies reveal organizational affiliations affecting provider decisions. Provider relationship mapping displays referral pattern analysis showing how care flows within markets.

Predictivenalytics and Optimization

AI-powered network design platforms explore 100+ configurations per network and product in a market, testing provider combinations against cost, quality, access, and member satisfaction objectives simultaneously. Machine learning algorithms recognize patterns in claims data forecasting future trends. Network gap prediction identifies emerging adequacy issues before regulatory violations occur. Provider recruitment targeting uses performance data recommending which providers to pursue based on strategic value rather than availability.

Interactive Dashboards and Visualization

Executive dashboards monitor network performance across key measures with real-time updates replacing quarterly static reports. Intuitive user interfaces enable insights in as little as three clicks eliminating need for data science expertise. Geo-spatial heat maps display provider distribution revealing geographic coverage gaps visually. Real-time performance monitoring with flexible trend analysis shows whether network changes deliver intended improvements.

Key Analytics Use Cases and Applications

Network Design and Optimization

Building high-performing networks that maximize medical cost savings while ensuring member access requires balancing competing objectives. Analytics platforms evaluate network resiliency by testing how well networks withstand provider departures, provider centrality showing which providers are critical connection points, and overall network strength quantifying competitive positioning. Creating tiered network strategies based on objective provider performance data enables value-based network designs steering members to high-performers.

Strategic Provider Recruitment

Identifying high-value providers for network expansion uses comprehensive performance data rather than reputation or relationships. Accelerating closure of network gaps focuses recruitment on actively practicing specialists addressing specific geographic or specialty shortfalls. Simulating potential provider impact on overall network performance before contracting prevents expensive mistakes adding providers who worsen rather than improve network metrics.

Leakage Prevention and Referral Optimization

Tracking referral volumes and trends identifies out-of-network leakage patterns showing where members leave network for care. Understanding where patient leakage occurs by specialty, geography, and condition enables targeted retention strategies. Optimizing referral patterns to keep care within network saves costs and improves care coordination. Analytics revealing why leakage occurs—whether from inadequate network, poor provider performance, or member preference—enables appropriate responses.

Regulatory Compliance Management

Eliminating “ghost providers” inactive in practice but listed in directories uses clinical activity insights proving providers haven’t treated patients recently. Ensuring compliance with federal and state network adequacy regulations requires continuous monitoring impossible manually. Automating network adequacy reviews with actionable market insights transforms compliance from manual burden to automated process. Analytics quantifying adequacy in real-time prevents violations before regulatory agencies identify deficiencies.

Value-Based Care Enablement

Assessing provider quality using NCQA HEDIS measures or CMS MIPS scores enables identification of high-performers for value-based contracts. Identifying providers contributing to 90th percentile quality performance reveals partners for risk-sharing arrangements. Supporting risk-sharing arrangements with performance transparency creates objective basis for shared savings calculations. Analytics tracking outcomes and costs enables continuous improvement in value-based programs.

Revenue Optimization

Using cost and quality metrics to build networks optimized for cost-effective care delivery reduces medical expenses while maintaining quality standards. Reducing unnecessary utilization through network design steering members to appropriate care settings improves margins. Increasing profitability through data-driven network refinement eliminates expensive, low-performing providers while adding high-value partners. Analytics quantifying network efficiency enables strategic decisions balancing growth, margin, and quality objectives.

The Analytics Technology Landscape

Enterprise Analytics Platforms

Comprehensive solutions offer network analytics as part of broader payer analytics suites integrating network, clinical, financial, and operational analytics. Leading platforms including Quest Analytics QES, MedeAnalytics Network Insights, CareJourney, and Milliman MedInsight provide enterprise-scalable solutions across all lines of business and specialties. These platforms offer end-to-end capabilities from data integration through advanced analytics and visualization.

Specialized Network Analytics Tools

Purpose-built solutions focus exclusively on provider network optimization with deep functionality in specific domains. McKinsey Network Designer provides AI-powered network optimization exploring hundreds of configurations. HealthWorksAI NetworkIntel offers Provider Network Scorecards for competitive positioning assessment. LexisNexis MarketView delivers competitive intelligence and market analysis. Specialized tools excel in specific use cases but may require integration with broader platforms.

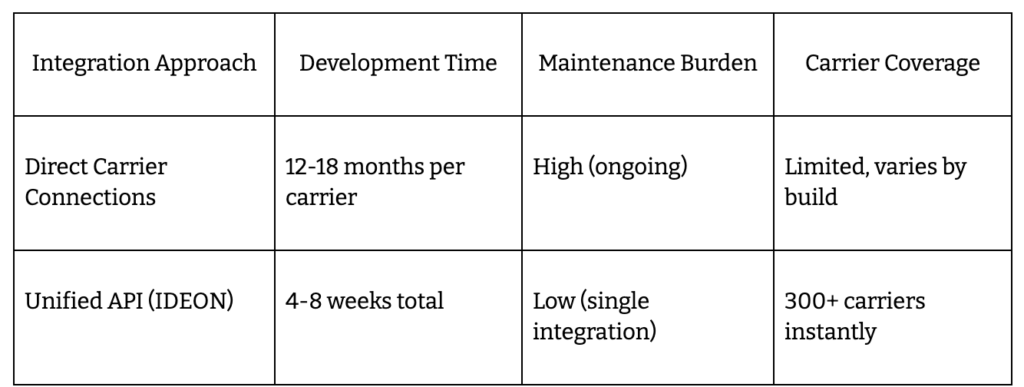

API-Enabled Data Infrastructure

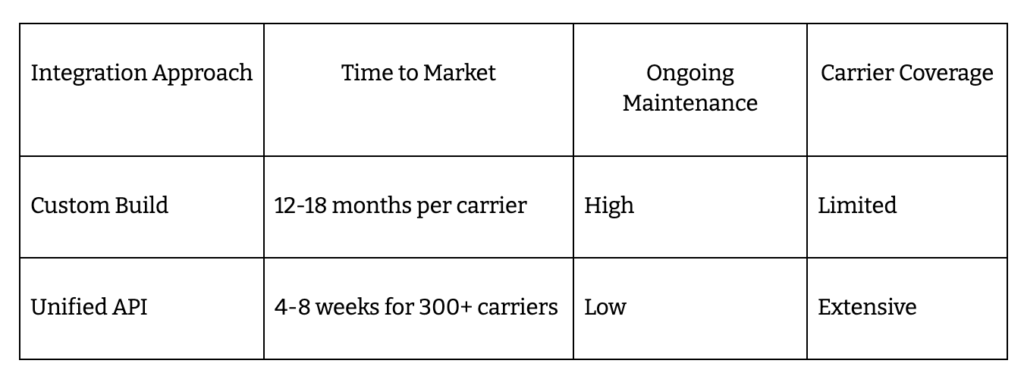

Real-time data access through unified API connections enables integration with existing healthcare IT systems including HRIS, claims platforms, and benefits administration tools. Normalized provider network data via standardized APIs accelerates analytics deployment by eliminating custom integration work. IdeonSelect provides comprehensive provider directories, network adequacy data, and specialty verification across 300+ carriers through unified API, creating data foundation essential for analytics applications without requiring carrier-by-carrier integration work consuming 12-18 months.

Data Sources and Integration

Proprietary claims databases covering all payer types and business lines provide analytical foundation. Third-party data integrations from trusted sources expand insights beyond internal claims. Provider cost transparency data from official reporting requirements enables accurate cost comparisons. Integration capabilities connecting internal and external data sources create comprehensive analytical views impossible with siloed data.

Organizations face infrastructure decision: build analytics capabilities internally requiring significant data engineering investment, AI/ML expertise, ongoing maintenance, and 12-18 months development time, or leverage existing platforms and API infrastructure deploying in weeks with subscription-based pricing and continuous vendor-managed updates. The build-versus-buy decision parallels network management itself—invest resources in undifferentiated infrastructure or focus on strategic network optimization.

Best Practices for Implementing Network Analytics

Start with Clear Objectives

Defining specific business problems analytics should solve focuses implementation on value delivery. Identifying key performance indicators including cost reduction targets, quality improvement goals, and adequacy compliance requirements establishes success metrics. Establishing baseline metrics for measuring improvement quantifies analytics value and justifies investment. Without clear objectives, analytics implementations produce reports without driving decisions.

Ensure Data Quality and Breadth

Access to comprehensive claims datasets covering Medicare, Medicaid, and Commercial populations provides foundational analytical capability. Prioritizing high-confidence data from multiple validated sources prevents garbage-in-garbage-out problems. Integrating proprietary organizational data with external benchmarks creates complete performance views. Data quality and breadth determine analytical accuracy and actionable insight generation.

Build Cross-Functional Teams

Combining network management, clinical, actuarial, and data science expertise ensures analytics addresses real business problems. Analytics insights must translate to actionable network strategies requiring operational expertise alongside technical capability. Fostering collaboration between technical and operational stakeholders prevents analytics existing in isolation from decision-making. Cross-functional teams bridge gap between data and action.

Leverage API Infrastructure

Using standardized provider data APIs accelerates analytics implementation by eliminating custom carrier integration work. Connecting analytics tools to real-time data sources rather than periodic batch feeds enables continuous monitoring. Continuous data updates versus quarterly refreshes transform analytics from historical reporting to forward-looking intelligence. API infrastructure provides data foundation enabling rapid analytics deployment.

Prioritize User Experience

Selecting platforms with intuitive dashboards requiring minimal training ensures adoption by non-technical users. Enabling self-service analytics for network managers eliminates bottlenecks requiring data science support for every question. Focusing on actionable visualizations over complex statistical reports drives decision-making rather than analysis paralysis. User experience determines whether analytics capabilities translate to business value.

Monitor and Iterate

Continuously evaluating analytics impact on network performance through before-after comparisons validates investment. Refining models based on outcomes and feedback improves accuracy over time. Expanding analytics use cases as organizational maturity grows maximizes platform value. Analytics implementations require ongoing optimization rather than one-time deployment.

How IdeonSelect Enables Network Analytics

IdeonSelect delivers normalized provider network data through unified API infrastructure, creating the data foundation essential for healthcare provider network analytics without requiring organizations to build hundreds of individual carrier integrations. The platform provides comprehensive provider directories, network adequacy validation, and specialty verification across 300+ insurance carriers, enabling analytics platforms to access clean, standardized provider data for performance analysis.

Technical Capabilities:

- Unified Data Access: Single API integration provides normalized provider data from 300+ carriers, eliminating custom carrier-by-carrier development requiring 12-18 months per integration

- Real-Time Updates: Automated refresh cycles ensure provider information reflects current network status without manual verification processes

- Comprehensive Provider Profiles: Practice locations, specialties, credentials, network status, panel capacity, and accepting new patients status across all connected carriers in standardized format

- Network Adequacy Data: Geographic coverage analysis, provider-to-member ratios, and specialty availability supporting compliance automation and adequacy analytics

- Analytics Integration: Clean, standardized data enabling analytics platforms to focus on insights rather than data acquisition and normalization

Measurable Outcomes:

- Weeks implementation instead of 12-18 months building carrier data integrations from scratch

- 300+ carrier coverage through single API versus individual integration efforts requiring massive engineering investment

- Standardized data format eliminating ETL complexity and data quality issues plaguing custom integrations

- Continuous updates managed by Ideon ensuring analytics operate on current rather than stale data

- Analytics acceleration enabling organizations to deploy network analytics rapidly by providing data foundation

IdeonSelect enables benefits platforms, TPAs, and health plans to deploy network analytics capabilities by providing the clean, normalized, comprehensive provider data required for meaningful analysis. Organizations focus analytics investments on deriving insights and optimizing networks rather than wasting resources on data acquisition infrastructure. This API-first approach transforms network analytics from multi-year data engineering projects into weeks-long analytical deployments.

The Future of Network Analytics

Advanced AI and Machine Learning

Increasingly sophisticated predictive models for network optimization will forecast member needs, provider performance trajectories, and market dynamics with greater accuracy. Automated recommendations for provider recruitment and contract negotiations will evolve from suggesting candidates to executing strategies. Natural language processing for unstructured data analysis including provider notes, member feedback, and contract terms will extract insights currently trapped in text.

Real-Time Analytics

Shift from periodic reporting to continuous monitoring will accelerate as streaming data architectures mature. Immediate alerts for network adequacy issues or provider performance changes will enable proactive responses before problems escalate. Live dashboards reflecting current network status will replace quarterly snapshots showing outdated information. Real-time analytics transforms network management from reactive to proactive discipline.

Integrated Care Coordination

Analytics linking network design to care management and population health will optimize entire care continuum. Member-provider matching based on outcomes data will improve satisfaction and clinical results. Closed-loop systems connecting insights to interventions will automatically route members to appropriate providers. Integration across network strategy, care management, and utilization management creates synergies impossible with siloed functions.

Transparency and Consumerism

Public-facing provider performance data will drive member choices as transparency requirements expand. Analytics supporting member decision tools and cost estimators will empower informed healthcare decisions. Increased focus on patient experience metrics in network evaluation will shift networks toward member-centricity. Transparency pressures will force networks to compete on objective performance rather than marketing.

Organizations leveraging advanced analytics optimize networks for better outcomes, lower costs, and equitable care—positioning themselves for competitive success in value-based healthcare landscape where performance determines financial results.

Final Words

Healthcare provider network analytics transforms raw claims data and provider information into strategic intelligence enabling optimized network composition, reduced medical costs, and improved member outcomes. Organizations implementing comprehensive analytics deliver measurable results including 10% medical cost reductions through strategic network design, faster network optimization exploring 100+ configurations in minutes rather than months of manual analysis, and improved regulatory compliance through continuous adequacy monitoring preventing violations before auditors identify issues.

Leading health plans already leveraging advanced analytics gain significant competitive advantages over organizations relying on manual spreadsheet-based network management. The performance gap widens as analytics-enabled organizations continuously refine networks using objective data while competitors make subjective decisions based on incomplete information and relationships. Analytics capabilities separate market leaders from laggards in increasingly competitive healthcare landscape.

Essential capabilities enabling network analytics success include comprehensive claims data covering Medicare, Medicaid, and Commercial populations, provider performance metrics measuring cost, quality, and satisfaction objectively, predictive modeling forecasting network gaps and optimization opportunities, and competitive intelligence revealing market positioning and strategic options. Organizations must decide: build analytics infrastructure internally requiring significant data engineering investment and 12-18 months development, or leverage existing platforms and API solutions deploying in weeks.

Assessing current analytics capabilities reveals baseline performance and improvement opportunities. Organizations processing millions of claims without extracting strategic insights waste valuable assets. Evaluating comprehensive analytics platforms including Quest Analytics, MedeAnalytics, CareJourney, Milliman MedInsight, and API infrastructure solutions like IdeonSelect provides comparison against build-from-scratch approaches. Starting with high-impact use cases including provider recruitment optimization, leakage prevention, or adequacy compliance demonstrates value quickly.

Building cross-functional teams translating analytics insights into network strategy ensures capabilities drive decisions rather than generating unused reports. Network management, clinical, actuarial, and data science expertise working collaboratively transforms analytics from technical exercise to strategic advantage. Organizations treating analytics as technology project rather than business transformation fail to realize value.

Advanced network analytics enables data-driven decisions replacing intuition and relationships with objective performance measurement, optimized provider networks balancing cost and quality rather than simply maximizing provider count, and superior member outcomes through strategic network design—essential capabilities for thriving in modern healthcare landscape where value-based c

FAQs: Healthcare Provider Network Analytics Essentials

Q: What is healthcare provider network analytics?

Healthcare provider network analytics is the systematic use of data science, statistical analysis, and business intelligence tools to evaluate provider network performance, optimize network composition, and improve healthcare delivery outcomes. It encompasses provider performance measurement across cost, quality, and satisfaction metrics, network utilization analysis revealing member access patterns, competitive intelligence comparing networks, predictive modeling forecasting gaps, and claims data analysis processing millions of transactions for actionable insights.

Q: How does network analytics differ from traditional network management?

Traditional network management relies on manual provider analysis, quarterly static reports, reactive problem-solving after issues surface, and spreadsheet-based tracking consuming staff time. Network analytics delivers automated insights through AI-powered algorithms, real-time dashboards showing current performance, proactive optimization identifying opportunities before problems occur, and self-service analytics enabling insights in three clicks rather than three weeks of manual work.

Q: What business results can organizations expect from implementing network analytics?

Organizations implementing comprehensive network analytics achieve typical 10% reduction in total medical cost through optimized network design balancing access, quality, and cost objectives. Advanced platforms enable building high-performing networks in minutes rather than months by exploring 100+ network configurations simultaneously. Analytics prevents regulatory compliance violations through continuous adequacy monitoring, improves member satisfaction through better provider matching, and enables strategic provider recruitment based on objective performance data.

Q: Which healthcare organizations use provider network analytics?

Health insurance payers including Medicare Advantage plans, commercial carriers, and Medicaid MCOs use network analytics for competitive positioning and cost management. Accountable Care Organizations managing provider performance under shared risk arrangements require analytics for value-based contracting. Benefits technology platforms including HR tech vendors and ICHRA administrators leverage analytics capabilities through API infrastructure. Provider organizations use network analytics to understand market position and negotiate contracts based on performance data.

Q: What are the core components of network analytics systems?

Core components include comprehensive claims data integration accessing Medicare, Medicaid, and Commercial datasets covering 300 million beneficiaries and 10 billion claims, provider performance analytics measuring cost efficiency and quality metrics, network adequacy and access analysis ensuring regulatory compliance, competitive intelligence revealing market positioning, predictive analytics and AI-powered optimization exploring network configurations, and interactive dashboards enabling self-service insights in as little as three clicks.

Q: How does network analytics support value-based care initiatives?

Network analytics enables value-based care by assessing provider quality using NCQA HEDIS measures or CMS MIPS scores, identifying providers contributing to 90th percentile quality performance for risk-sharing arrangements, supporting transparent performance measurement enabling objective shared savings calculations, and tracking outcomes and costs enabling continuous improvement in value-based programs. Analytics provides objective foundation for provider performance discussions replacing subjective assessments.

Q: What analytics use cases deliver the highest impact?

High-impact use cases include network design and optimization building high-performing networks maximizing medical cost savings while ensuring access, strategic provider recruitment identifying high-value providers based on performance data, leakage prevention tracking referral patterns keeping care within network, regulatory compliance management automating adequacy reviews, value-based care enablement identifying quality performers, and revenue optimization reducing expenses through data-driven network refinement.

Q: How does API infrastructure accelerate network analytics implementation?

API infrastructure provides real-time data access through unified connections to provider data sources, eliminating custom carrier integration work requiring 12-18 months per connection. Standardized provider data APIs deliver normalized information across 300+ carriers enabling analytics platforms to focus on insights rather than data acquisition. IdeonSelect provides comprehensive provider directories and network adequacy data via unified API, creating data foundation essential for analytics without requiring custom integration development.

Q: What should organizations consider when selecting network analytics platforms?

Evaluation criteria should emphasize data quality and breadth ensuring access to comprehensive Medicare, Medicaid, and Commercial claims datasets, AI sophistication enabling predictive modeling and automated optimization, user experience providing intuitive dashboards requiring minimal training, integration capabilities connecting to existing systems through APIs, scalability handling growing data volumes without performance degradation, and vendor domain expertise in healthcare analytics versus generic business intelligence tools.

Q: What is the recommended approach for starting network analytics adoption?

Organizations should start by defining specific business problems analytics should solve and establishing baseline metrics for measuring improvement. Access to comprehensive claims datasets covering all payer types provides analytical foundation. Starting with high-impact use cases including provider recruitment optimization, leakage prevention, or adequacy compliance demonstrates value quickly. Building cross-functional teams combining network management, clinical, actuarial, and data science expertise ensures insights translate to actionable strategies.

Q: How does the build-versus-buy decision work for network analytics?

Organizations face infrastructure choice: build analytics capabilities internally requiring significant data engineering investment, AI/ML expertise, ongoing maintenance, and 12-18 months development, or leverage existing platforms and API infrastructure deploying in weeks with subscription-based pricing and continuous vendor-managed updates. Internal builds require solving data acquisition, normalization, analytics algorithm development, and visualization challenges. Platform approaches provide comprehensive capabilities immediately with continuous improvements.

Q: What future capabilities are emerging in network analytics?

Emerging capabilities include increasingly sophisticated AI and machine learning for predictive modeling and automated recommendations, real-time analytics replacing periodic reporting with continuous monitoring, integrated care coordination linking network design to population health management, natural language processing extracting insights from unstructured data, and transparency tools supporting member decision-making with public provider performance data. Industry transformation toward value-based care accelerates analytics sophistication requirements.

Explore Ideon's IdeonSelect for health plans and benefits platforms

Ready to take the next step? See how Ideon works.